Personal finance is an area of life that every adult must manage. It can be intimidating but with the right tips, it is completely manageable. No matter where you in your life right now, you can manage your personal finances like a pro. All it takes is some understanding of how to go about it, and commitment to improving the areas that need help. In this blog post, I’m going to share 7 tips that will help you to manage your personal finances like a pro.

Note: This page contains affiliate links, which means that if you buy something using one of the links below, I may earn a commission.

7 Tips to Manage Your Personal Finances Like a Pro

Managing your personal finances doesn’t all have to be boring or time-consuming. Even if you’re working with a small budget, when you are realistic about your situation and truthful with yourself, you can come up with a plan that will work for your needs.

Let’s get started…

(1) Create a Budget

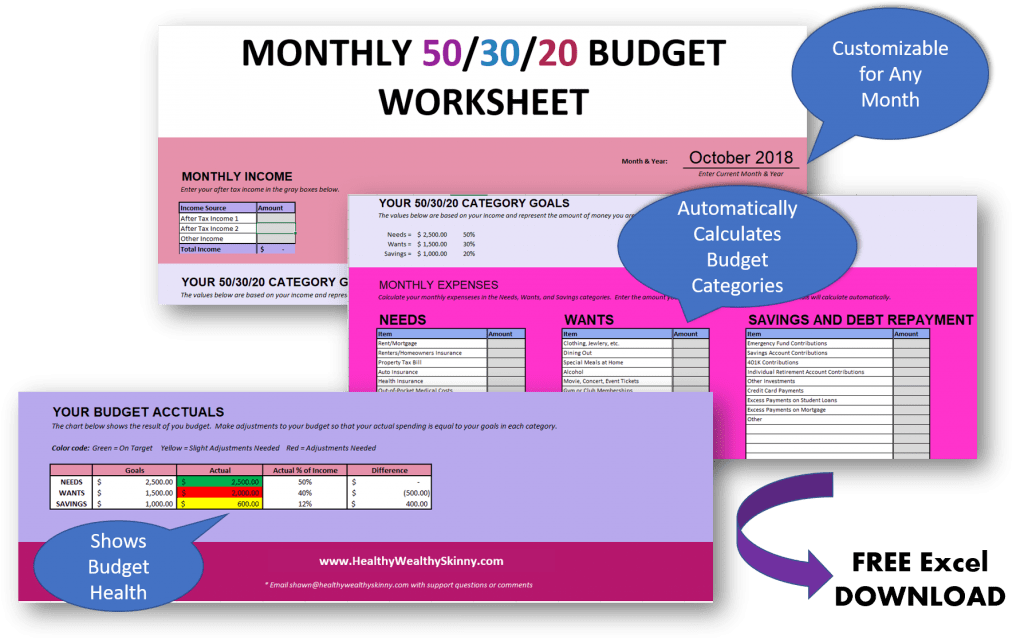

The first step to managing your personal finances is to set up a realistic budget for where you are right now. There are multiple tools available to help you create and manage your budget. You can use a printable budget worksheet, an app, or a simple spreadsheet to create your budget. Some banks also have budgeting features built into their online banking applications.

Here are a few popular budgeting apps:

Download a copy of our free Monthly 50/30/20 Budget Worksheet. It’s a free excel spreadsheet to help you create and maintain your budget.

Choose the tool that is the easiest for you. For some, this might be keeping a budget notebook. The tool you use isn’t important. The steps to developing a budget are essentially the same no matter the method.

Step 1: Write Down Your Net Income

When creating your budget you want to focus on your Net Income. Your Gross Income is the amount you make before deductions. When it comes to your budget, you shouldn’t focus on what you make before deductions such as health insurance, taxes, and your retirement savings contribution. Use your net income, because it represents the actual amount of money you have to work with.

What you make before those deductions doesn’t really matter when creating a budget because you cannot spend any of that money that you don’t receive.

Step 2: Track Your Spending

For about a month, track your spending habits. The only way to get real with yourself is to write down everything you spend money on – whether it’s cash, credit, or a debit card. It doesn’t matter if it’s one buck or 100 bucks; you need to track it and categorize it.

List all your fixed expenses first. These are items that cannot be adjusted like your rent, mortgage, car payment, utilities and so forth.

Then make a separate list with variable spendings such as eating out, entertainment, groceries, and gas. If you want to do this fast, you can look at your past records on your bank statements and credit card accounts to organize it all.

Step 3: Set Goals

You need to set some financial goals that you want to accomplish before you continue. You should have some short-term goals for the next year or two, some mid-term goals for the next five to ten years, and then long-term goals such as saving for retirement. Use real dollar amounts that are real numbers with realistic deadlines or target dates.

Step 4: Write Down a Plan

Now that you know what you earn, what you spend, and what your goals are for now and the future, it’s time to write down a plan. You may realize as you’re developing the plan that you need to cancel your cable, drop to a cheaper mobile plan, or adjust your desires based on wants versus needs. You need gas to get to work, but you don’t need to watch six hours of TV each evening. There are many ways to stretch your budget. Determine what needs to be cut to meet your goals.

Step 5: Adjust as You Go

It can take a few months to perfect your budget as you navigate your life and goals. Don’t go for short-term pleasure by buying that $300 purse if it’s going to take away your ability to save for that vacation you want to take next year.

Don’t give up anything you need for a temporary want. But, at the same time, you want to still enjoy life and not make it all a drudge. Find things that you can do that cost less but still give you an enjoyable life.

(2) Start an Emergency Fund

One of the best defenses against job loss, illness, and other problems is an emergency fund. An emergency fund is money set aside that is in a normal bank account that you can access quickly. For example, if your car breaks down, that is when you’ll use your emergency fund.

Why Have an Emergency Fund?

If you have an emergency fund, you’ll be much less likely to end up relying on credit cards – which can often just make your life worse when you’re in the middle of a crisis. An emergency fund will eliminate the need for you to use debt for these life challenges.

How Much Should I Have in My Emergency Fund?

How much you save in your emergency fund honestly depends on your financial situation. It depends on how much money you earn, how hard it will be for you to replace that income, and other issues.

But, most experts say at least six months of living expenses (after you cut out all unnecessary spending) is a good start. If you have a business, you should try to save about 18 months’ expenses so that you don’t go out of business.

Where Should I Put My Emergency Fund

You should just put it in your regular bank account so that it can be accessed easily with a debit card or a quick transfer of funds. Most credit unions offer the ability to have a checking account and a savings account without any fees.

If you can find a high yield savings account that has few penalties for withdrawals and is insured by the FDIC, that’s a good choice.

How Do I Build My Emergency Fund?

First, you need to add it to your budget. Consider this expense a mandatory fixed amount. If you can have it withheld from your pay, so much the better as you’ll never look at it.

Every time you get a raise you can add this amount to either your emergency fund or your long-term savings, and you won’t notice it.

Keep your change in a jar and when it’s full, take it to the bank. Put all savings from coupons into savings. If you spend less than your budget on any given pay period, move that to your savings.

If you have nothing for savings, find places to cut expenses so that you can build an emergency fund. If you must, get an extra job or become an independent contractor to add some income to your fund. If you get a tax refund, save it in your emergency fund every single year.

The more seriously you take saving money in your emergency fund, the better off you will be. Even if all you can manage to save is the same amount as your insurance deductibles (health, car, and house), you’ll end a lot of stress and avoid using credit for things that are going to happen. Cars break, people get sick, and houses get damaged by storms. It’s all part of life.

(3) Limit Your Debt

One of the biggest factors in financial issues people face is debt. People from all income brackets tend to have too much debt. Even if you’re a six-figure earner, you may have debt that is causing you to feel broke. It’s important to limit the amount and type of debt you take on.

Good Debt and Bad Debt

There is both good debt and bad debt. An example of good debt is a mortgage for a reasonably sized house in a reasonable neighborhood. Bad debt is pretty much any type of unsecured consumer debt like credit cards, especially if you used that credit card for entertainment and not an emergency.

The important thing is to be realistic about how much debt you can take and stick to the budget you’ve created. Banks will often base how much they give you for a mortgage limit based on your gross income instead of net income. This is dangerous because your net income does not represent the actual amount of money you have to spend.

Debt-to-Income Ratio

There is something that financial planners use to determine if you have too much debt. It’s called DTI (Debt-to-Income Ratio). This is figured out by adding up your total debt payments for each month and then dividing it by your full monthly income.

If you earn $3500 a month and have total debts of $2000 a month, your DTI is 2000/3500= 57%. As a note to remember, a DTI over 43% can keep you from qualifying for a mortgage or other loans. You want to shoot for a DTI of between 18% and 36% according to the professionals.

Control Your Use of Credit Cards

Speaking of debt, let’s talk a little about credit cards. Credit cards can be a great thing in terms of buying power, respect, and even discounts.

Some cards can earn you cashback and get you added protection if you use them correctly. But for some people, even using the credit card once can be the beginning of a personal financial disaster.

Monitor Your Credit Score

It’s important to keep tabs on your credit score too. Use a system like CreditKarma.com, which is free to sign up for, and keep an eye on your credit. It does not affect your credit to do this.

However, be aware that they pay for their service by using credit card advertisements, and if you can’t say no, it’s best to avoid this and send for your free yearly report from each of the three credit reporting firms. You can learn more about this by visiting the Federal Trade Commission’s Website.

Pay off Student Loans

Let’s talk a little about student loans, separately from other types of debt. Student loans are an investment in your earning future or the earning future of your kids. First, don’t get loans in your name for your children. Even Suze Orman would agree.

She says that the best gift you can give your children is your independence when you’re elderly and getting loans for your child’s education doesn’t make financial sense.

So, what we’re talking about here is your own personal student loan debt. There is a lot to consider regarding student loans.

It’ll require some financial projection to ensure that you do it right. Today, student loans offer many different types of payment plans. You can pay based on your income, and you can pay based on the regular 10-year payment plan to get it paid off.

(4) Buy Life Insurance

One reason financial planning is so important is your family. Whether it’s your spouse, your kids, or your parents, it’s imperative that you consider them in all your planning. The best way to do that is to buy life insurance.

You don’t have to leave a big inheritance to your family when you pass, but you don’t want to leave a mess behind. Have enough life insurance to take care of your family’s needs and pay final expenses. The rule of thumb is that the younger your family, the more insurance you need.

Don’t think that stay-at-home parents don’t need life insurance either; many times they need to be covered for more than the working partner because of all the benefits they provide to the family such as childcare, cooking, cleaning and more.

First, assess whether you need life insurance at all. Some people really don’t need it. If you have adequate savings to cover your final expenses and keep your family out of poverty, then you don’t need life insurance.

To determine how much life insurance you need, answer the following questions:

- How much debt do you have?

- How much do you spend each month?

- How much do you save each month?

- How much income do your survivors need if you’re gone?

- How much can you earn on your money?

- How much inflation do you expect?

All these factors come into play. Let’s just pull a number out of thin air and say that your family needs an income of about $3000 a month to stay right where they are without anything changing other than that you are gone.

How much insurance do you need to provide that? If you can earn 5% a year on an investment, that means you’d need to buy a life insurance policy that provides about an $800K payout such that you could easily provide $3000 a month to your family after you’re gone.

Keep in mind that the younger you are, the less expensive it is to buy the insurance, and the cheaper it’ll be until you’re older.

If all you can afford is a burial policy (assuming you have no savings), then that is at least something and one less thing for your family to have to worry about. Financial planning should start when you’re young if possible.

(5) Plan and Save for Your Retirement

One thing you shouldn’t overlook is planning and saving for your retirement. It’s very easy to say when you’re young that you won’t ever retire, but you may need to.

Your job may be killed off due to technology, you may develop illnesses and be unable to work, or you may change your mind and decide you’d rather spend your golden years traveling than working. At the very least, start saving now for retirement so that you have a choice.

Tips for saving for retirement:

Maximize Your Employer Contributions – If you have a job with a retirement savings plan, invest the maximum amount that the company matches. If they match up to 5% of your income, you should donate 5% of your income.

Open Your Own IRA – You can easily open your own IRA through your credit union or via another method. Donate the maximum amount you’re allowed by law. You may want to talk to a financial planner to help you with this. Most credit unions offer some financial planning free with your account.

Set Up Direct Deposit – Don’t make yourself think about it too much. Once you’ve set your intentions and budget for your retirement savings, do it automatically so that you never think about it again. Just set it up and forget it. Don’t micromanage it or try to figure it out.

You can also contribute to bonds, CDs, and other investments but if you do nothing else, use your employer’s system and an individual retirement account via your credit union based on the year you want to retire, and your projected needs based on your budget and your credit union’s recommendations.

(6) Minimize Your Tax Liability

A very important part of financial planning is managing your tax liability. Depending on your situation, it may pay to see a financial planner. As mentioned before, most credit unions have financial planners on staff who can help you.

The important thing is to hire a professional to help you who is honest and ethical. But, also teach yourself what you need to know so that you don’t just leave it to them.

It’s too important to let other people do everything for you, because sometimes you may run into someone who seems legit but who is really trying to scam you.

Check out everyone who offers to help you make a lot of money or who wants to help you manage your finances. Only go to reputable places to find people to help.

(7) Live Your Best Life

One thing to keep in mind about budgeting is that you aren’t guaranteed tomorrow. Chances are you will live to about 80, but most financial planners say to plan to live to 99 years old. But, you could get sick tomorrow. You could die tomorrow.

It’s better to balance how you invest and save with how you live your life. Just live within your means and if you don’t like the means, then you must find a way to increase your earnings to fit the lifestyle you want to live – while still taking care of tomorrow.

Get more education, start a side gig, and truly experience life as it’s meant to be with lots of rich experiences with people you love.

Don’t give up amazing experiences and live a life full of drudgery and work just to have retirement savings. Find a balance that gives you joy now and security later.

You will be happy you did it when you’re 80, and you’ll live a full and happy life if you find the right balance between wants and needs.

Leave a comment and share your personal finance tips.

Pin the Pin to Your Finance or Money Pinterest Boards

Don’t forget to Like, Share, Tweet, and Pin this post.

Great post! I wish I could organise according to all of your tips. Well done ?

Thanks Kristine!

It’s so important to have emergency money put back for when things go wrong last minute! Planning ahead for the future is a must!

So true Allie. An emergency fund gives you peace of mind.

Great tips! My husband and I are currently working on eliminating student loans and working towards saving for retirement as well as life insurance. At least we’re getting started. Thanks for sharing

Hey Rhonda! Sounds like you guys are well on your way.

I have been trying to take better control of my finances now that I’m in my 30s. I first started with my credit, as my identity was stolen and credit cards were opened in my name. It’s been a slow process, but it’s been working. I now need to build my emergency fund.

Great advice! x

Michelle

dressingwithstyle-s.com

Sorry to hear you were a victim of identity theft. I’ve heard it’s so hard to recover from that. Keep pushing and you will get back on track.

This is so useful! I’m good at budgeting and saving but definitely going to work on having an emergency fund ?

Hey Lucy! If you a good a saving then you’ve got the hard part covered.

Thanks for such an informative article. Many people are confused between debit and credit. You have explained it very well. Also, I write on a similar niche, could your please share your views on it here: Bookkeeping Fee Structure

Thanks Gena! Will do!